On June 21, at the 2025 SMM (4th) Electric Drive System Conference & Drive Motor Industry Forum - eVTOL Electric Drive System Forum, jointly hosted by SMM Information & Technology Co., Ltd., Hunan Hongwang New Material Technology Co., Ltd., Louxing District People's Government, and the National-level Loudi Economic and Technological Development Zone, Li Gang, Deputy General Manager of the Low-Altitude Economy Division at Rudong Information Technology Services (Shanghai) Co., Ltd. and a certified expert from the China Federation of Logistics & Purchasing (CFLP), shared his insights on "Rethinking the Challenges of the Low-Altitude Economy Industry Chain and Data Management."

I. Connotation and Strategic Value of the Low-Altitude Economy

Concept Definition and Industry Landscape

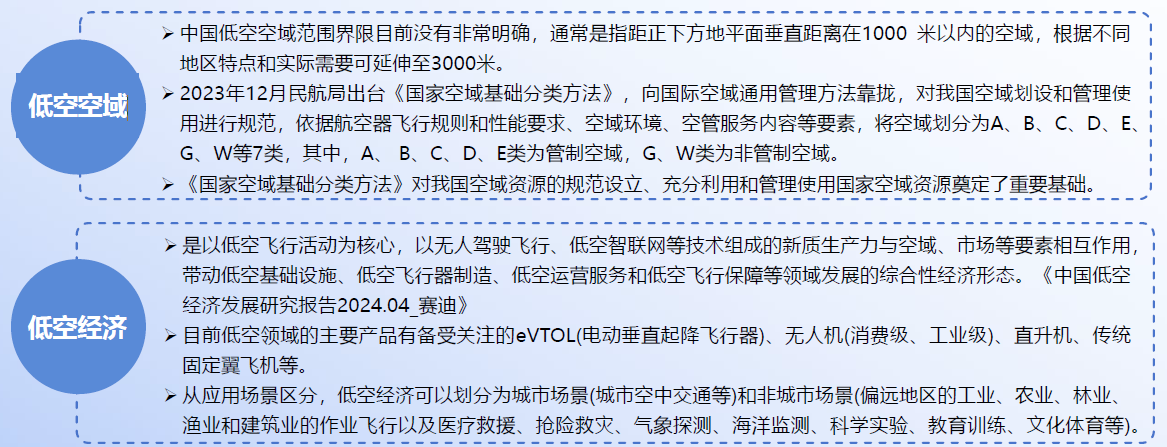

• The low-altitude economy is a comprehensive economic form driven by various low-altitude flight activities involving manned and unmanned aircraft, which radiate and promote the integrated development of related industries.

• The low-altitude economy relies on low-altitude airspace, with general aviation as the leading industry, featuring strong driving effects and a long industry chain. It is closely integrated with high-tech fields such as scenario innovation, new material applications, and artificial intelligence.

• The low-altitude economy is widely reflected in the primary, secondary, and tertiary industries, playing an increasingly important role in promoting economic development, strengthening social security, and serving national defense undertakings.

• The essence of developing the low-altitude economy at present: transforming low-altitude elements into scenarios and scenarios into economic value.

• Characteristics of the low-altitude economy: It is an industry chain-based economy with multi-domain, cross-industry, and full-chain characteristics. It integrates new-type low-altitude production and service methods with traditional general aviation formats, relying on information and digital management technologies. The development of the low-altitude economy plays a crucial role in promoting economic development, strengthening social security, and serving national defense undertakings.

Main Categories of Low-Altitude Airspace Flights

• Low-altitude passenger and cargo transportation: Whether it is manned or cargo transportation using fixed-wing aircraft or helicopters, it offers significant advantages such as flexibility, convenience, efficiency, and accuracy, making it an important tool for future urban and rural transportation and rapid logistics. Vertical takeoff and landing drones will be the primary means for the last-mile delivery of rapid cargo transportation in mountainous, remote, and sparsely populated areas.

• Low-altitude operational flights: Such as industrial construction operations, smart agriculture, airborne medical instruments, spraying systems, aerial remote sensing systems, and hanging systems.

• Aviation emergency rescue: Ensuring safety, rapidity, and accessibility.

• Low-altitude tourism and leisure: Emphasizing safety, practicality, and economy.

The low-altitude economy will become an important engine for new growth in the national economy

It will become a new growth point for high-quality development of China's national economy in the 21st century

• China has 689 general aviation enterprises, with 3,173 registered general aviation aircraft and 451 general airports. In 2023, there were 1.357 million hours of operational flights, with an average annual growth rate of over 12% in the past three years.

• There are approximately 2,000 UAV design and manufacturing units, over 20,000 operating enterprises, and more than 1.3 million domestically registered UAVs, with 23.11 million hours of flight time.

• In 2023, the scale of China's low-altitude economy reached 500 billion yuan, and it is expected to exceed 2 trillion yuan by 2030.

Global Layout and Competition in the Low-Altitude Economy

Overall, China and the US are the most advanced in the development of the low-altitude economy. The US has accumulated rich aviation experience through its vast general aviation industry and affiliated sectors, particularly holding significant advantages in areas such as route planning and aircraft design. China shares similar advantages with the US in general aviation and unmanned aerial vehicle (UAV) sectors. Meanwhile, China enjoys a late-mover advantage in developing the low-altitude economy, enabling rapid infrastructure deployment tailored to the characteristics of low-altitude flight.

Current Status of Domestic Low-Altitude Economy Development

• Against the backdrop of new quality productive forces, the central government's top-level design and relevant policies are vigorously promoting the deepening of airspace reform, with the continuous emergence of new aircraft, and strategic emerging industries driving new momentum for domestic demand.

• The concept of the domestic low-altitude economy is not a recent one. As early as 2010, the central government had proactively planned reforms for China's low-altitude industries and airspace. After 2022, the pace of policy rollouts significantly accelerated, with the synergy of basic research, product implementation, and policy guidance providing fertile ground for the implementation and rapid development of the low-altitude industry.

National Airspace Management Pilots Progressing Orderly, with Potential for Further Expansion in the Future

• The reform process of airspace management directly impacts the prosperity and development of the low-altitude economy. In December 2023, the National Air Traffic Control Commission organized the formulation of the "National Airspace Basic Classification Method," adding Class G airspace below a true altitude of 300 meters and Class W airspace below a true altitude of 120 meters, providing legal low-altitude airspace for eVTOLs, light and small UAVs, and general aviation. In November 2024, the Central Air Traffic Control Commission announced the launch of eVTOL pilots in six cities: Hefei, Hangzhou, Shenzhen, Suzhou, Chengdu, and Chongqing.

• The pilot documents include relevant planning for routes and regions, with airspace below 600 meters authorized to some local governments. The first batch of pilot provinces and cities for the low-altitude economy possess obvious advantages in terms of geographical location, natural conditions, economic foundation, industrial support, and policy environment, providing strong support and guarantees for the development of the low-altitude economy.

• In the future, with the further improvement of policies and sustained market growth, these regions are expected to achieve more significant results in the low-altitude economy. It is anticipated that the second batch of pilot cities will be announced soon, and the utilization rate of domestic low-altitude airspace is expected to improve.

II. Key Elements and Infrastructure of the Low-Altitude Economy

Key Elements of Low-Altitude Economy Development

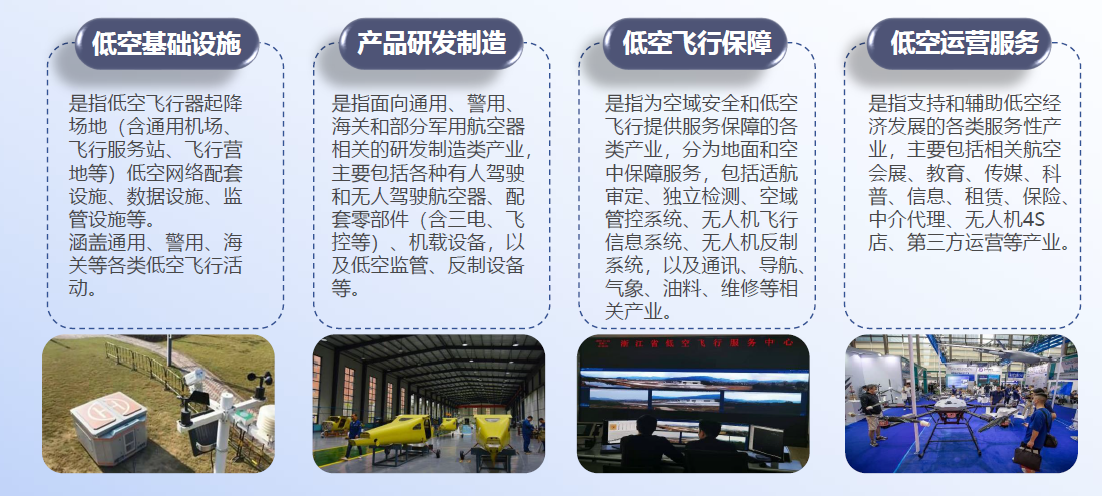

From an industrial perspective, the key elements of low-altitude economy development mainly include low-altitude infrastructure, product R&D and manufacturing, low-altitude flight support, and low-altitude operation services, characterized by wide radiation, long industry chains, strong growth potential, and significant driving effects.

The three main development avenues for the low-altitude economy: "Three New" Initiatives

Reference is made to the "Research Report on the Development of China's Low-Altitude Economy (2024)" by the China Center for Information Industry Development (CCID) under the Ministry of Industry and Information Technology (MIIT), which elaborates on the "new" infrastructure, "new" scenarios, and "new" equipment for low-altitude activities.

Advancement of Four-Network Integration

It provides an introduction from the perspectives of facility networks, air route networks, air connectivity networks, and service networks.

►Advancement of Four-Network Integration in the Low-Altitude Economy: Facility Networks

Facility Networks: These are the physical infrastructure of the low-altitude economy, including low-altitude takeoff and landing stations, connecting facilities, energy stations, emergency alternate landing sites, parking facilities, maintenance facilities, and flight test sites. They provide hardware support for low-altitude flights, ensuring flight safety, efficiency, and convenience. They are the foundation for the widespread application of new-type aircraft such as electric vertical takeoff and landing (eVTOL) vehicles, and their improvement helps enhance low-altitude flight service capabilities.

►Advancement of Four-Network Integration in the Low-Altitude Economy: Air Connectivity Networks

Air Connectivity Networks: These are critical information infrastructure that meet the needs for low-altitude sensing and communication. They encompass communication facilities, navigation facilities, surveillance facilities, and meteorological facilities. They utilize digital means to achieve comprehensive sensing, real-time monitoring, and precise control of low-altitude flights, improving flight safety and providing support for flight data collection, analysis, and application. With the application of 5G-A integrated sensing and communication technology and the Beidou Navigation Satellite System, communication capabilities, navigation accuracy, and surveillance range continue to improve.

►Advancement of Four-Network Integration in the Low-Altitude Economy: Air Route Networks

Air Route Networks: These are navigation support infrastructure that include low-altitude digital airspace maps, airspace representation, digital twins, 3D maps, knowledge bases, and rule bases. They provide precise navigation and planning services for low-altitude flights, ensuring accurate and efficient flights, simplifying flight approval processes, and improving the utilization efficiency of airspace resources. As the future air traffic management system continues to improve, the role of air route networks will become even more important.

►Advancement of Four-Network Integration in the Low-Altitude Economy: Service Networks

Service Networks: These are digital management and service systems and comprehensive supervision platforms, mainly including low-altitude monitoring systems, low-altitude flight service systems, and low-altitude flight control systems. They are customer-oriented, meeting regulatory safety and corporate flight requirements, providing a comprehensive supervision service platform, and achieving one-stop management of flight services. Through digital means, they coordinate, manage, and allocate low-altitude flights, supporting various low-altitude flight activities, improving flight safety and reliability, and providing support for the optimization and upgrading of flight services. In the future, they will develop towards a "one-stop" direction.

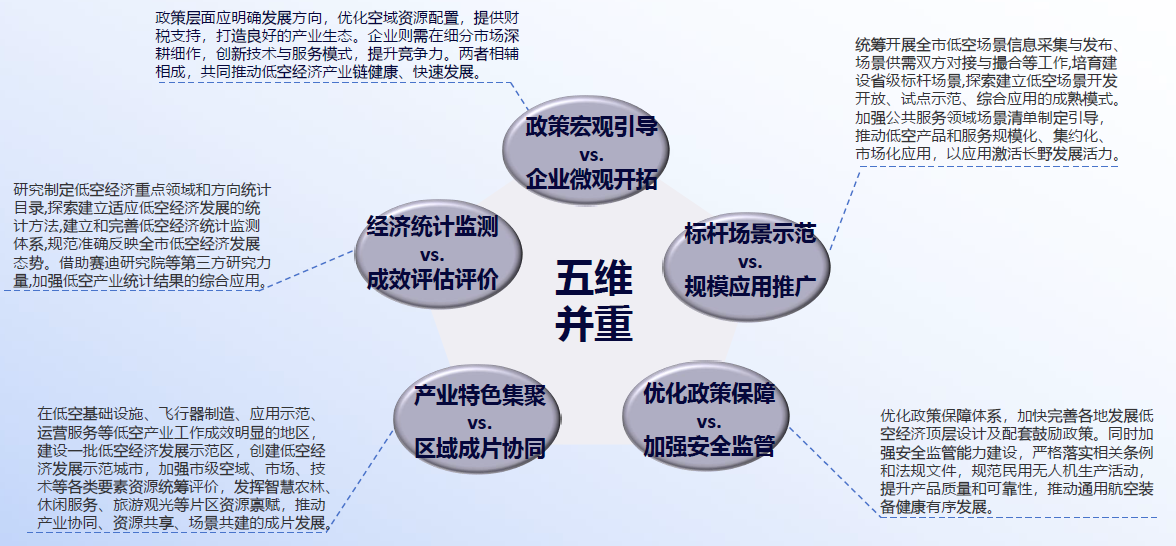

The development of the low-altitude economy industry chain requires a holistic approach: Five-Dimensional Emphasis

III. Pain Points and Breakthrough Paths for the Development of the Low-Altitude Economy

1. The policy and regulatory framework is not yet complete or well-suited

• The safety regulatory framework in terms of regulations needs improvement, and there is a significant demand for regulatory tasks. Due to the rapid development of the low-altitude economy and the increasing frequency of low-altitude flight activities, the number of regulatory targets and tasks has surged, posing challenges to safety regulation. Additionally, relevant laws and regulations have not been promptly developed or updated. In the case of drones, existing legal norms lack specificity and adaptability, with gaps or overlaps in some regulatory areas, leading to inefficient regulation. Current regulations mostly follow traditional aviation standards and are unable to accommodate new business models such as drones and eVTOLs.

• There is a limited number of laws and regulations related to low-altitude flight. The low-altitude economy encompasses a wide range of scenarios and sectors, with diverse and complex legal needs. It is necessary to establish legislative norms and leadership mechanisms to clarify the responsibilities of various parties, formulate standardized industry standards, and ensure the implementation of regulations.

2. Core technology bottlenecks constrain industrial autonomy

The low-altitude economy is vigorously reshaping the modern transportation and industrial landscape, ranking alongside artificial intelligence as new quality productive forces and being seen as a new blue ocean for future economic growth. In the drone sector, China holds a leading global position. However, behind the seemingly broad development prospects, bottlenecks in core technology areas such as autonomous navigation and low-altitude communication act as invisible barriers, constraining the safe and healthy development of the low-altitude economy. For example:

Navigation systems: Deficiencies in complex environmental perception, low efficiency in multi-drone coordination, and insufficient reliability of navigation signals.

Low-altitude communication: Structural deficiencies in network coverage and intense competition for spectrum resources.

Composite materials: In terms of carbon fiber, over 90% of high-strength carbon fiber above T800 grade relies on imports from Toray T1100G (Japan) and Hexcel IM10 (US). Domestic T800-grade capacity accounts for only 8% of the global total.

Core chips: Specialty chips for high-end models, such as IMU, inertial navigation systems, and high-precision gyroscopes, still mainly rely on imports. For example, TDK.

3. Supporting infrastructure construction is severely lagging

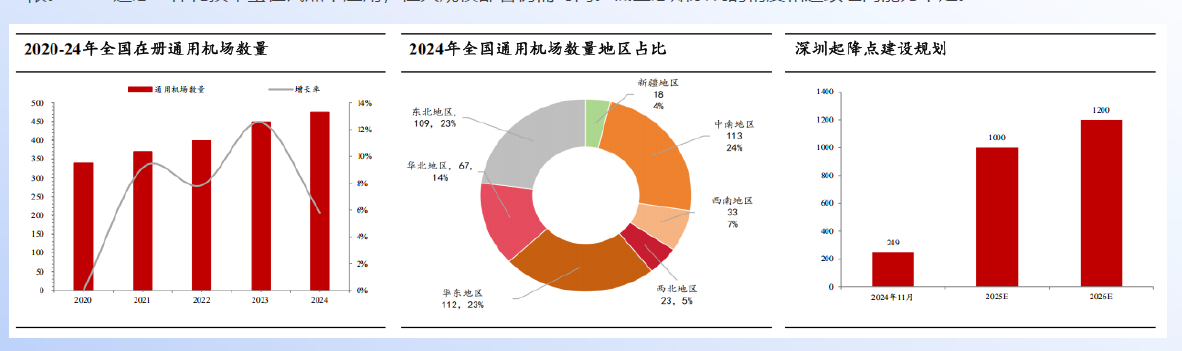

• The construction of low-altitude flight infrastructure is relatively lagging. Both the number of general aviation airports and drone takeoff and landing sites, as well as the land area required for constructing general aviation airports and takeoff and landing sites, are insufficient to meet the rapidly growing demand of the low-altitude economy.

• The number of general aviation airports is inadequate, and their geographical distribution is uneven. As of 2024, China has 475 general aviation airports. Compared with European and American countries, both the number and density of general aviation airports in China are low, and the supply of infrastructure such as takeoff and landing sites for low-altitude aircraft is insufficient to meet low-altitude demand. Meanwhile, there are significant regional disparities in the distribution of general aviation airports in China. These airports are mainly concentrated in economically developed regions in Central-South and Eastern China, while the number of general aviation airports in Western China is relatively small. In 2024, there were 74 general aviation airports in Western China, accounting for only 16% of the total.

• There is a lack of coordinated planning in facility construction. Most takeoff and landing sites are built by enterprises themselves, making it difficult to share them and resulting in resource waste. Taking Shenzhen as an example, in order to rapidly deploy takeoff and landing sites, most of them are built by enterprises themselves. However, the construction standards of different operators have not yet been unified, making it impossible to achieve functional compatibility and reuse. Takeoff and landing sites owned by enterprises or individuals lead to duplication and resource waste. In the future, the government will build takeoff and landing sites with public attributes through joint construction by state-owned enterprises and private enterprises.

• Technically, the communication system is not yet mature. Low-altitude flight requires high-precision navigation, real-time communication, and dynamic sensing capabilities. However, most existing communication base stations are designed for ground scenarios, with limited air coverage. Although 5G-A integrated sensing and communication technology has been applied in pilot projects, large-scale deployment still takes time. The accuracy and continuous networking capabilities of low-altitude sensing systems are insufficient.

4. Rigid Airspace Management Mechanisms

• To promote an efficient airspace management system nationwide, it is necessary to establish a unified digital foundation and collaborative management platform, which involves interest coordination and data sharing among different regions and departments, making implementation difficult.

• In terms of technology, although advanced technologies such as digital twins are available, how to further improve the real-time performance, reliability, and intelligence level of the system to cope with increasingly complex low-altitude flight scenarios still requires continuous R&D and innovation.

• In addition, with the rapid development of the low-altitude economy, higher requirements are placed on the flexibility and adaptability of airspace management. The existing management models and technical means need to be continuously optimized and upgraded, forming a nationwide network with unified standards (currently, there are no unified standards).

5. The Market Environment for Low-Altitude Operation Services Urgently Needs Guidance and Cultivation

• The low-altitude operation segment is the most core segment driving the sustainable growth of the low-altitude economy. Currently, China's low-altitude operation service market is not yet mature, with market entities still relatively weak, and the market structure needs further optimization and adjustment.

• According to incomplete statistics, affected by factors such as unstable demand and small market size in the traditional general aviation market, most traditional general aviation operation enterprises in China have suffered losses and have not yet developed a mature commercial profit model. Related flight activities are mainly for training purposes, with consumer flight services accounting for a relatively low proportion. There is a significant gap compared to the more than 60% proportion of consumer flight services in countries such as the United States and Europe. In the civilian UAV market, the application market for light and small UAVs is relatively fragmented, while most large and medium-sized UAVs, eVTOLs, and other new-type low-altitude aircraft have not yet been commercialized due to airworthiness progress.

6. Persistent Shortage of Professional Talent

➢ Significant gap in interdisciplinary talent: There is an urgent demand for technical professionals in aviation manufacturing, flight operations, maintenance support, and other fields, while the education and training system remains inadequate.

➢ Insufficient R&D talent: High-end technologies (such as flight control systems and composite materials) rely on imports, and the development of independent innovation teams lags behind.

➢ Severe shortage of airworthiness certification and service support personnel: Currently, there are over 2,000 aircraft models awaiting airworthiness certification, while China's supporting airworthiness certification personnel team numbers around 400 (approximately one-tenth the size of the US). According to relevant institutions, at the current pace of airworthiness certification, it would take 300 years to process all existing applications!

7. High Initial Development Costs, Economic Viability Remains Distant

➢ The industry chain is still immature, with high costs at every stage from R&D, materials, and production to airworthiness certification. Taking eVTOL as an example, EHang's EH216-S unmanned electric vertical take-off and landing ("eVTOL") aircraft has an official guidance price of $410,000 per unit (2.39 million yuan per unit) in global markets outside China. Additionally, as some companies enter the airworthiness certification and commercialization phases, the required funding may still reach hundreds of millions or even billions of yuan.

➢ The lengthy airworthiness certification process hinders mass production. According to China's regulations, any entity or individual designing civil aircraft must apply for and obtain a Type Certificate (TC) from the Civil Aviation Administration; manufacturing civil aircraft requires production permit approval and a Production Certificate (PC); and operating civil aircraft requires single-aircraft airworthiness inspection and an Airworthiness Certificate (AC). Furthermore, before a specific aircraft model can be officially deployed for commercial operations, an Operating Certificate (OC) is required. In current eVTOL airworthiness certification practices, each project is handled on a case-by-case basis, with dedicated conditions separately formulated for each. Under prolonged airworthiness certification, companies cannot achieve mass production, costs remain high, and commercialization is still a distant goal.

8. Lack of Environmental Impact Assessment for Low-Altitude Flight Activities

➢ Prominent noise pollution

Urban air mobility increases noise loads in residential areas, and existing noise reduction technologies do not provide full coverage.

➢ Challenges in battery recycling

The disposal system for discarded lithium batteries is inadequate, posing high risks of heavy metal pollution.

➢ Unquantified ecological interference

There is a lack of life cycle environmental assessment standards, and insufficient research on impacts such as bird migration and ecologically sensitive areas.

IV. Discussion on Challenges and Countermeasures in Data Management of the Low-Altitude Economy

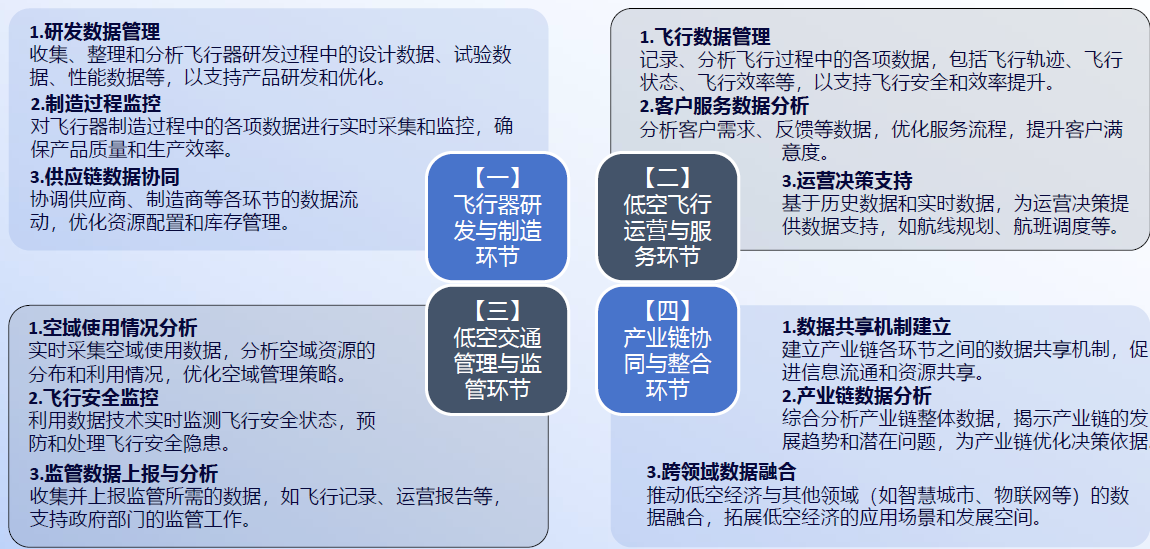

Data management runs through every link of the low-altitude economy industry chain.

The development of the low-altitude economy has a high demand for and reliance on digital technology, as it possesses the characteristic of "inherent full digitization."

The healthy and sustainable development of the low-altitude economy cannot be achieved without the support of data management.

➢ For the low-altitude economy, professional data management is not an option but a necessity.

➢ Data management is of great significance to the development of the entire industry chain of the low-altitude economy. By strengthening work in data collection and integration, processing and analysis, application and services, as well as security and privacy protection, the healthy development of the low-altitude economy industry chain can be promoted, and continuous industrial innovation and upgrading can be achieved.

Common Challenges Faced by Data Management in the Low-Altitude Economy

1. Rapid Growth in Data Volume

With the rapid development of technologies such as the Internet and the Internet of Things, data volume has grown exponentially, placing immense pressure on data storage, processing, and analysis.

2. Data Diversity and Complexity

Data is no longer limited to structured data; semi-structured and unstructured data are increasingly prevalent. Processing these complex and diverse types of data requires more advanced technologies and tools.

3. Data Quality Issues

The accuracy, completeness, and consistency of data are core issues in data management. It is necessary to ensure data quality to support effective decision-making analysis.

4. Data Security and Privacy Protection

With the widespread application of data, data security and privacy protection have become significant challenges, necessitating the establishment of comprehensive security mechanisms and privacy protection measures.

5. Shortage of Technology and Talent

Data management requires advanced technological support and a professional talent pool, but currently, there is a prominent shortage of both technology and talent in the market.

Special Challenges Faced by Data Management in the Low-Altitude Economy

1. Complexity of Airspace Management

The low-altitude economy involves complex airspace management issues, including flight path planning, airspace allocation, and conflict resolution, which require refined data management and analysis for support.

2. High Requirements for Flight Safety

Flight safety is a core issue in the low-altitude economy industry. Data management needs to ensure the real-time nature, accuracy, and completeness of flight data to support flight safety monitoring and early warning.

3. Uncertainty in Regulations and Policies

The low-altitude economy industry is still in its early stages of development, and relevant regulations and policies are not yet perfect, which brings significant uncertainty and risks to data management.

4. Challenges in Cross-Domain Data Integration

The low-altitude economy industry involves data from multiple domains, including aviation, communications, and geographic information. Achieving the integration and sharing of cross-domain data is a challenging task.

5. Lack of Infrastructure Construction, Data Standardization, and Interoperability

Currently, the data collection, data distribution, and other infrastructure conditions of the low-altitude economy industry are in their infancy. Both static and dynamic data lack unified data standards and interoperability mechanisms, leading to widespread data silos and making it difficult to achieve data sharing and effective utilization.

Discussion on Data Management Based on the Uniqueness of Low-Altitude Economy Development

1. Prioritize the Promotion of Infrastructure Construction for Low-Altitude Economy Data Management

The foundational constructions necessary for the development of the low-altitude economy industry must take precedence, with priority given to ground support facilities, network security facilities, communication and navigation networks, data centers and cloud platforms, low-altitude flight service systems, and air traffic control systems. Relevant departments should guide various market entities to actively participate.

2. Establish a Unified Data Management Platform

To achieve unified management and analysis of low-altitude economy data, a centralized data management platform should be established. This platform should have functions such as data collection, storage, processing, and analysis, and be able to provide customized data services for different users. Leveraging the first-mover advantage in the early stages of the new-type industry, a solid foundation should be laid in areas such as data standards, data distribution and circulation, and data accountability mechanisms.

3. Place Greater Emphasis on Data Quality and Security

Ensuring the accuracy and reliability of low-altitude economy data is crucial. A strict data quality control mechanism should be established to clean, validate, and standardize the data. Meanwhile, data security protection should be strengthened by adopting technical means such as encryption and access control to prevent data leakage and misuse.

4. Promote Data Sharing and Openness in the Low-Altitude Economy

The low-altitude economy industry chain involves multiple industrial domains, including aircraft manufacturing, operational services, and application scenarios. Data management should focus on promoting data integration and sharing among different industries while safeguarding data security and privacy, breaking down data silos, and achieving data interoperability.

5. Strengthen Technological R&D and Talent Cultivation

In response to the special needs of low-altitude economy data management, relevant technological R&D and innovation should be strengthened. Meanwhile, a professional talent team that understands the low-altitude economy, comprehends business scenarios, is proficient in data management, and possesses data analysis and security assurance capabilities should be cultivated to provide strong professional support for the sustainable development of the low-altitude economy.

V. Policy Recommendations and Future Outlook

Six-Party Synergy for Integrated Development of the Low-Altitude Economy Industry

➢ To develop the low-altitude economy, it is necessary to integrate "government, industry, academia, research, application, and finance," strengthening the "six-party synergy."

➢ Establish a low-altitude economy support system with Chinese characteristics, characterized by government leadership, enterprise-driven operations, market orientation, and the highly integrated and synergistic collaboration of six key elements.

A Unified Blueprint: Top-Level Design and Systematic Planning

➢ The "unified blueprint" emphasizes the need for a unified top-level design to clarify the development direction, goals, and technological pathways of the low-altitude economy, avoiding redundant construction and resource waste. Its core lies in formulating a long-term plan that covers the entire industry chain, encompassing key areas such as airspace management, infrastructure construction, R&D, and the expansion of application scenarios.

➢ National-level coordination: The National Development and Reform Commission (NDRC) has established a Low-Altitude Economy Development Department to promote the implementation of policies such as airspace stratification management and the designation of primary flight corridors. For example, the "Low-Altitude Economy Development Roadmap" clearly outlines the goal of achieving airspace stratification management below 3,000 meters by 2025.

➢ Significance: Through top-level design, it addresses the fragmentation of airspace management, ensuring the efficient utilization of low-altitude resources and the overall coordination of the industrial ecosystem.

A Unified Strategy: Cross-Regional and Cross-Departmental Collaboration

➢ The "unified strategy" requires breaking down administrative divisions and industry barriers, achieving resource integration, standardization, and benefit-sharing through a unified coordination mechanism, thereby forming a nationwide development synergy.

➢ Military-civilian-local government collaboration: Establish a tripartite cooperation mechanism among the military, local governments, and civilians. For instance, Inner Mongolia has promoted low-altitude airspace opening through a joint military-civilian-local government airspace management model.

➢ Regional linkage: The Chengdu-Chongqing economic circle jointly develops airspace resources, while Beijing and Tianjin promote legislative coordination and the joint construction of industrial systems.

➢ Industry collaboration: Build a system that integrates "a unified network in the sky and a unified strategy on the ground," combining ground facilities such as general aviation airports and UAV bases with low-altitude flight networks.

》Click to view the special report on the 2025 SMM (4th) Electric Drive System Conference & Drive Motor Industry Forum